The scale of the problem is hard to overstate. Javelin Advisory Services reported $15.6 billion in U.S. ATO losses in 2024, up from $12.7 billion the prior year, with 5.1 million consumer victims and an average loss of $2,575 per victim. ATO attempts against consumers surged 250% in the same period—and 42% of victims closed the affected account entirely.

For organizations that handle customer accounts, employee credentials, or sensitive data, understanding how ATO works, how to investigate it, and how to prevent it is not a cybersecurity nicety. It is a core operational requirement.

Key Takeaways

- ATO fraud gives attackers control of a legitimate account—most often through stolen credentials, phishing, or malware

- Top attack vectors include credential stuffing, phishing, SIM swapping, keyloggers, and AiTM phishing kits

- Key warning signs: unexpected account changes, failed logins from unfamiliar locations, unrecognized devices, and unexplained transactions

- Investigation starts with immediate evidence preservation, log analysis, and mapping the full attack chain

- Prevention requires layered defenses: phishing-resistant MFA, behavioral monitoring, credential hygiene, and dark web monitoring

How ATO Fraud Works: Attack Methods and Stages

ATO typically unfolds in three phases. First, the attacker compromises credentials. Second, they conduct quiet reconnaissance—small account changes that go unnoticed. Third, full exploitation begins. Attackers often remain undetected for weeks because their early actions mimic legitimate user behavior.

Mandiant's M-Trends 2025 report found the global median attacker dwell time rose to 11 days in 2024, with email phishing accounting for 39% of cloud compromise initial vectors and stolen credentials at 35%.

Credential Stuffing and Brute Force

Credential stuffing works because most people reuse passwords. Attackers purchase leaked username-password pairs from dark web marketplaces and deploy automated bots to test them across dozens of platforms simultaneously. The math is on their side: SpyCloud's 2025 Annual Identity Exposure Report found that 70% of users exposed in breaches reused previously exposed passwords across other accounts.

Brute force attacks follow a different logic: trial-and-error scripts cycle through password combinations until one works. Short, simple passwords fall quickly. Hive Systems' 2025 Password Table shows that numeric-only passwords of common lengths can be cracked almost instantly with modern GPU hardware.

Phishing, Vishing, and Social Engineering

Phishing remains the most reliable initial access vector. Attackers craft convincing emails, SMS messages, or fake login pages that trick targets into surrendering credentials directly. Business and government accounts are increasingly targeted with spear-phishing tailored to the victim's specific role and organization. Two variants are growing fast:

- Vishing (phone-based social engineering) — CrowdStrike reported a 442% increase in vishing between H1 and H2 2024, driven by generative AI tools that lower the skill barrier for attackers

- Deepfake-assisted impersonation — The FBI warned in May 2025 that malicious actors were impersonating senior U.S. officials using AI-generated audio, making voice-based deception increasingly difficult to detect

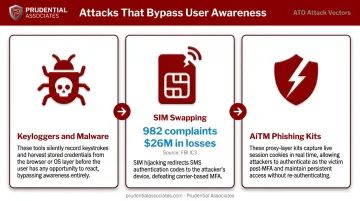

Infrastructure-Level Attacks: Malware, SIM Swapping, and AiTM

These attacks bypass user awareness entirely, operating at the infrastructure level before any visible sign of compromise appears:

- Keyloggers and malware — Installed via infected email attachments, untrusted app downloads, or drive-by browser exploits, these silently capture keystrokes and transmit credentials to the attacker without any visible sign of compromise

- SIM swapping — Attackers socially engineer mobile carriers into transferring a victim's phone number to a new SIM card, neutralizing SMS-based two-factor authentication; the FBI IC3 recorded 982 SIM swap complaints and nearly $26 million in losses in 2024

- Adversary-in-the-middle (AiTM) phishing kits — These intercept authentication sessions in real time, stealing session cookies that allow attackers to authenticate on behalf of the user even when MFA is active; Microsoft documented one AiTM campaign that targeted more than 10,000 organizations

The Real Costs of ATO Fraud and Warning Signs to Watch For

Financial loss is only the most visible consequence. When ATO goes unaddressed, organizations face:

- Regulatory penalties under GDPR (72-hour breach notification), HIPAA (60-day notification for breaches affecting 500+ individuals), and PCI-DSS

- Long-term reputational damage — 42% of ATO victims close the affected account, which means permanent customer churn

- Legal liability from negligent security practices or delayed notification

- Operational disruption from account recovery, fraud disputes, and incident response costs

Understanding these costs makes early detection a business priority, not just a security checkbox. The signals below help you identify an attack before it escalates.

Warning Signs You're Under Attack

Watch for these indicators across both individual accounts and broader organizational patterns:

Individual account indicators:

- Sudden changes to account credentials, contact details, or payment beneficiaries you didn't make

- Failed login attempts from unfamiliar IP addresses or geographic locations

- Login activity from unrecognized devices or at abnormal hours

- Unexplained transactions, new payees, or withdrawal attempts

Organizational indicators:

- Multiple users requesting password resets within a short time window

- A spike in transaction disputes or chargebacks across accounts

- Unusual API call volumes or automated login patterns in access logs

The organizational indicators deserve close attention. A single anomalous login is easy to dismiss as user error — but when the same pattern repeats across multiple accounts simultaneously, you're likely looking at an active, coordinated campaign rather than coincidence.

Investigating ATO Fraud: A Step-by-Step Process

Once ATO is suspected, the investigation needs to be both fast and methodical. Speed limits ongoing damage; methodology preserves the evidence needed for legal proceedings, insurance claims, and regulatory submissions. This is where cybersecurity expertise and law enforcement-style forensic discipline must work together.

Step 1: Contain and Preserve

The immediate priority is isolating the compromised account without destroying log integrity. This means:

- Suspending or isolating the affected account(s) through controlled access restriction—not deletion

- Avoiding immediate shutdown of connected systems, which can destroy volatile data such as running processes, memory-resident malware, and active command-and-control connections

- Physically isolating affected endpoints from the network by removing wired connections or disabling wireless interfaces in a controlled sequence

- Securing all systems and logs before any remediation steps alter the evidence state

Every action taken during containment must be documented. Chain of custody begins at first contact—not when the forensic team arrives.

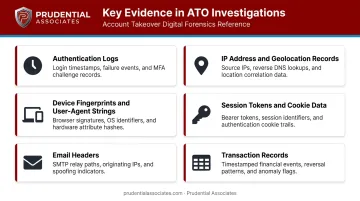

Step 2: Collect and Analyze Digital Evidence

Investigators gather and correlate evidence across multiple systems to reconstruct the attacker's timeline. Key evidence types include:

- Authentication logs with timestamps and session identifiers

- IP address and geolocation records

- Device fingerprints and user-agent strings

- Session tokens and cookie data

- Email headers from any phishing communications

- Transaction records and account change histories

Log correlation across endpoints, cloud platforms, and mobile devices is essential. Gaps in logs, or logs that have been cleared, are themselves evidentiary findings.

Certified examiners using tools such as EnCase (EnCE-certified), Cellebrite, Magnet Axiom (MCFE-certified), and forensic write-blocking hardware perform forensically sound acquisitions — cryptographic hashing ensures evidence is unchanged from the point of collection and remains defensible in court.

Prudential Associates' team holds certifications including CISSP, CEH, EnCE, GCFA, CFCE, and CCME, and their examiners have testified as expert witnesses in state and federal courts — including the firm's CEO, who has provided expert witness testimony in over 500 court appearances.

Step 3: Trace the Attack Chain and Identify the Breach Point

Investigators work backward from the exploitation point to identify the initial access vector. The central questions:

- Was entry gained through phishing, a credential dump, malware, or an insider?

- Which accounts were accessed, and in what sequence?

- What data was viewed, copied, or exfiltrated?

- Were any funds moved, and through what channels?

The attack chain analysis determines the full scope of compromise. That scope directly shapes both the recovery plan and the regulatory notification obligations that follow.

Step 4: Notify Stakeholders and Coordinate Response

Once scope is established, notification is not optional—it is legally required in most scenarios involving personal, financial, or health data. Key timelines:

- GDPR: Supervisory authority notification within 72 hours of discovery

- HIPAA: Affected individuals notified within 60 days; HHS notification for breaches affecting 500+

- FTC Safeguards Rule: FTC notification within 30 days for events affecting 500+ consumers

Prudential Associates assists corporate clients and legal counsel with regulatory notification guidance, evidence preservation, and expert witness support for resulting litigation or regulatory proceedings. Their forensic examiners have authored declarations and affidavits, participated in depositions, and provided expert guidance on legal motions — covering both the technical and legal dimensions of ATO response.

How to Prevent Account Takeover Fraud

No single control stops ATO. The organizations that fare best treat prevention as a compounding stack of controls, where each layer catches what the others miss.

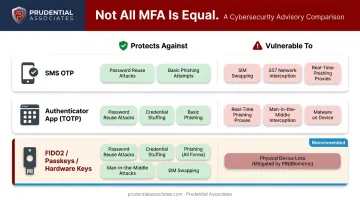

Implement Phishing-Resistant Multi-Factor Authentication

Microsoft research found MFA reduced account compromise risk by 99.22% overall—but not all MFA is equal.

| MFA Type | Protects Against | Vulnerable To |

|---|---|---|

| SMS one-time passcodes | Password-only attacks | SIM swapping, AiTM |

| Authenticator app TOTP | SIM swapping | AiTM phishing kits |

| FIDO2 / passkeys / hardware keys | SIM swapping, AiTM, phishing | Physical device theft |

CISA designates FIDO2/WebAuthn/passkeys as the strongest available MFA and notes that phishing-resistant options are the only form that meaningfully resists AiTM attacks. Enable the strongest available MFA on all accounts—prioritize privileged and financial accounts first.

Deploy Behavioral Monitoring

Behavioral monitoring tools analyze continuous signals, including typing cadence, device fingerprint, login geolocation, session duration, and transaction patterns, flagging deviations automatically. This works passively, without adding friction to legitimate users. Prudential Associates' MDR service provides early detection aligned to this model, identifying threats before they escalate.

Enforce Credential Hygiene

Credential stuffing succeeds because users reuse passwords across accounts. Closing that gap requires:

- Enforce unique, complex passwords across all accounts

- Implement a credential manager to eliminate reuse at scale

- Run regular checks against known breach databases — NIST SP 800-63B requires verifiers to screen proposed passwords against lists of compromised values

- Force credential resets immediately when exposure is detected

Conduct Security Awareness Training

Security awareness training targets the human vector. Phishing and social engineering remain the dominant initial access methods, so employees who can recognize a spear-phishing email, an MFA fatigue push-bombing attempt, or a suspicious voice call represent one of the highest-ROI investments in ATO prevention.

Prudential Associates' training programs cover phishing, social engineering, mobile computing risks, and incident reporting, with a recurring cadence to keep pace as attack techniques evolve.

Apply Risk-Based Authentication

Risk-based authentication adjusts verification requirements dynamically based on context. Rather than applying maximum friction universally, verification scales with the actual risk of each session:

| Session Context | Risk Level | Response |

|---|---|---|

| Known device, normal hours | Low | Standard MFA |

| New device, normal location | Medium | Step-up verification |

| New device, unfamiliar country, high-value transaction | High | Additional verification + alert |

This balances security with user experience: friction scales with risk, not with every login.

Long-Term ATO Defense Strategies

Sustained ATO prevention depends on systemic controls built into standard operations — not reactive fixes applied after an incident:

- Audit access privileges regularly — Remove dormant accounts and over-permissioned credentials to shrink the attack surface; credentials that aren't used can still be stolen and exploited

- Monitor the dark web proactively — Prudential Associates' dark web monitoring scans marketplaces, forums, paste sites, and encrypted platforms for exposed credentials. Real-time alerts trigger forced resets before an attacker can act on stolen data

- Test your incident response plan — Define escalation paths, notification templates, and forensic investigation protocols for ATO scenarios specifically; teams that have rehearsed their response move faster and make fewer mistakes when it matters

- Coordinate with law enforcement when warranted — For cases meeting the threshold for criminal referral, Prudential Associates' examiners include former law enforcement professionals with established agency relationships. They can facilitate coordination with federal and state investigators while maintaining appropriate legal protections

Conclusion

ATO fraud has identifiable attack methods, predictable warning signs, and a documented prevention and investigation playbook. Organizations that build layered controls—starting with phishing-resistant MFA and credential hygiene, supported by behavioral monitoring and proactive dark web intelligence—substantially reduce both their likelihood of compromise and the damage if it occurs.

When an attack does happen, the investigation must be immediate, methodical, and forensically defensible. Evidence that isn't properly preserved can't support litigation, insurance claims, or regulatory submissions. The difference between a standard IT response and a forensic investigation comes down to chain of custody, evidentiary standards, and the ability to produce findings that hold up in court or before a regulator.

Prudential Associates provides that forensic capability. Operating since 1972, the firm combines former FBI, CIA, and law enforcement investigative backgrounds with more than 30 professional certifications and an in-house laboratory equipped for court-ready evidence handling. Corporate clients, legal counsel, and government agencies engage the firm across every phase of ATO response: initial triage, forensic examination, regulatory documentation, and expert witness testimony.

Frequently Asked Questions

What are the red flags for account takeover fraud?

Common indicators include:

- Unexpected changes to account credentials, contact details, or payment beneficiaries

- Failed login attempts from unfamiliar IP addresses or locations

- Login activity from unrecognized devices or at abnormal hours

For organizations, a sudden spike in password resets or transaction disputes across multiple accounts often signals a coordinated campaign.

What evidence is required to prove account takeover fraud?

Key evidence includes authentication logs, IP address and geolocation records, device fingerprints, session tokens, email headers, and timestamped records of account changes. All of this must be preserved in a forensically sound manner (using write-blocking and cryptographic hashing) to remain admissible in legal or regulatory proceedings.

Do banks investigate account takeover fraud claims?

Banks typically conduct internal investigations when fraud is reported, reviewing transaction records and login data. For complex cases or those heading toward litigation, victims should also engage independent forensic investigators who can preserve evidence properly and support legal proceedings the bank's internal process will not address.

What is an example of account takeover fraud?

A fraudster purchases leaked credentials on the dark web, uses credential stuffing bots to access a victim's online banking account, adds a new payee, and transfers fundswithin hours. The legitimate account holder may not notice until a transaction alert or a failed login attempt prompts them to check.

What should I do immediately if my account has been taken over?

Alert the account provider and lock the account immediately. Change passwords on any other accounts sharing the same credentials. Review recent transactions and preserve all related notifications or communications. Report losses to your financial institution and, if significant, file a complaint with the FBI's IC3.

How is ATO fraud different from identity theft?

ATO involves taking control of an existing account using stolen credentials. Identity theft typically involves using stolen personal information to open new accounts or impersonate the victim in other ways. ATO can become a gateway to broader identity theft if the attacker harvests personal data from the compromised account, such as Social Security numbers, dates of birth, or security question answers.