Introduction

Divorce law in every U.S. state requires both spouses to fully disclose all assets and liabilities. This is a legal duty, and violating it constitutes fraud against both the court and the other spouse.

Yet asset concealment happens. According to a 2025 Bankrate survey, 40% of Americans in committed relationships admit to keeping a financial secret from their partner. When that secrecy carries into divorce proceedings, courts cannot divide marital property fairly — and the uninformed spouse may walk away with significantly less than they're legally entitled to.

This guide covers everything you need to identify and address hidden assets:

- Warning signs that a spouse may be concealing wealth

- The most common concealment tactics used in divorce

- A step-by-step process for uncovering what's been buried

- Professional tools and forensic resources available to you

- Legal consequences for a spouse caught hiding assets

Key Takeaways

- Both spouses are legally required to disclose all assets during divorce — concealment is a serious legal violation, not just a breach of trust

- Common hiding tactics include secret bank accounts, cryptocurrency wallets, underreported business income, fake debts, and transfers to family members

- Formal legal discovery tools — interrogatories, subpoenas, and depositions — compel full financial disclosure

- Forensic accountants and digital forensics specialists routinely surface assets standard discovery misses

- Courts can penalize the concealing spouse with sanctions, fee awards, unequal asset splits, or criminal charges

Warning Signs Your Spouse May Be Hiding Assets

Spouses who plan to hide assets typically start months before filing — which means early detection gives you time to preserve documents and build your case. Watch for these patterns.

Behavioral and Financial Red Flags

- Sudden financial secrecy: password-protecting accounts, redirecting mail, refusing to discuss finances

- New accounts, credit cards, or loans you weren't told about

- Large unexplained cash withdrawals or transfers to unfamiliar accounts

- Newly claimed debts owed to friends, family members, or business associates

- Underreporting lifestyle expenses while claiming financial hardship

The ACFE's matrimonial tracing guidance flags recurring ATM withdrawals, transfers to undisclosed accounts, and unusually large transactions as priority items for forensic review — patterns that also often surface in lifestyle analysis.

Lifestyle vs. Income Discrepancies

When a spouse's spending — travel, vehicles, renovations, gifts — doesn't match their reported income or claimed financial hardship, that gap signals underreported income. Courts and forensic accountants call this a lifestyle analysis, and it consistently surfaces discrepancies that reported figures miss.

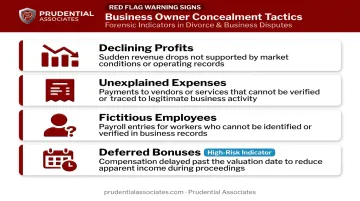

Business-Specific Warning Signs

Self-employed spouses and business owners have more opportunities to manipulate reported figures on financial documents. Watch for:

- Declining reported profits that coincide with the start of divorce proceedings

- Unexplained business expenses or new vendor relationships

- Sudden new "employees" added to payroll (often fictitious or complicit family members)

- Deferred bonuses or commissions that happen to be paid after the divorce is final

Common Ways Spouses Hide Assets in Divorce

Recognizing the method helps target the right investigative approach. Here are the most frequently encountered concealment tactics.

Underreporting Income and Manipulating Business Records

Self-employed spouses and business owners can delay sending invoices, defer bonuses, route income through shell companies, pay fictitious employees, or obtain deliberately low valuations of business interests. The goal is to shrink the apparent marital estate before the court sets a valuation date. These manipulations leave traces in tax filings, bank records, and payroll systems — traces that forensic review can surface when records are properly subpoenaed and cross-examined.

Secret and Offshore Accounts

Undisclosed domestic bank or investment accounts are among the most common concealment methods. Offshore accounts in jurisdictions with strict financial privacy laws add complexity, but both leave financial trails. Subpoenas to banks, cross-referencing loan applications against disclosed accounts, and credit report analysis can surface accounts a spouse never voluntarily mentioned.

Cryptocurrency and Digital Asset Wallets

Cryptocurrency is increasingly used as a concealment vehicle because it's perceived as anonymous. It isn't. Blockchain transactions are permanently recorded on public ledgers, and specialists can connect holdings to a specific individual through:

- Wallet identification and on-chain transaction analysis

- Exchange subpoenas to match account holders to wallet addresses

- Blockchain analytics platforms that reconstruct transfer histories

Courts across multiple jurisdictions now require disclosure of virtual currency transactions and current holdings — a reflection of how seriously the legal system treats this asset class.

Transferring Assets to Third Parties and Creating Fake Debts

A spouse may "gift" cash or property to a parent, sibling, or business partner with the understanding it will be returned post-divorce. Alternatively, they may fabricate loans owed to associates — creating paper liabilities that reduce the apparent marital estate. Both tactics involve a paper trail between parties that forensic review can identify.

Purchasing and Undervaluing Physical Assets

Cash purchases of collectibles, artwork, jewelry, or equipment are easy to omit from disclosures. For assets that do get disclosed, deliberately low appraisals of real estate or business interests can artificially deflate their contribution to the marital estate. Independent appraisals and auction records can contradict these valuations.

Step-by-Step: How to Find Hidden Assets in Divorce

Uncovering hidden assets requires a combination of personal documentation, formal legal tools, and professional expertise. The earlier you start, the harder it becomes for assets to disappear.

Step 1: Gather and Preserve Financial Records Immediately

Before your spouse knows you're considering divorce, collect:

- Tax returns for the past 3–5 years (federal and state)

- Bank and brokerage statements for all known accounts

- Credit card statements

- Loan applications — these are especially valuable because borrowers inflate assets when seeking credit

- Business financial records, including P&L statements and payroll records

- Property documents: deeds, titles, mortgage statements

Photograph, scan, or make copies of anything accessible. Once proceedings begin, access to shared accounts may become contested.

Step 2: Review Financial Records for Discrepancies

Compare what your spouse reports in divorce disclosures against what appears in prior-year tax returns, loan applications, and bank records. Look for:

- Large unexplained withdrawals or transfers in the months before filing

- Accounts or assets listed in loan applications that never appeared in divorce disclosures

- Income figures that don't match the lifestyle you shared

- New business entities or deductions that appeared recently

Even minor discrepancies are worth flagging. A $30,000 income drop the year before filing is rarely coincidental.

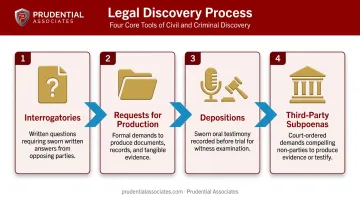

Step 3: Use the Formal Legal Discovery Process

Discovery is the legal mechanism that compels disclosure. The four core tools:

- Interrogatories — Written questions your spouse must answer under oath

- Requests for production — Compels delivery of specific financial documents

- Depositions — Sworn oral testimony from your spouse, their accountant, business partners, or other relevant parties

- Subpoenas to third parties — Banks, employers, investment firms, and cryptocurrency exchanges can be legally required to produce records directly, bypassing your spouse entirely

Florida Family Law Rules (Rules 12.340, 12.350, 12.351, and 12.410) codify all four tools, and Rule 12.380 authorizes sanctions for failure to comply. Similar mechanisms exist in every state.

Step 4: Engage a Forensic Accountant

Forensic accountants go beyond what standard discovery can compel. Their work typically includes:

- Reconstructing income streams obscured through business accounts or deferred payments

- Tracing money through complex transactions and shell entities

- Analyzing business valuations for understated worth

- Quantifying lifestyle-versus-reported-income discrepancies

Their analysis is admissible in court, and they can testify as expert witnesses to explain findings to a judge.

Under California Family Code § 1101, courts can order the concealing spouse to pay attorney's fees and investigation costs — meaning the innocent spouse may not bear the financial burden of exposing the fraud.

Step 5: Work with a Private Investigator or Digital Forensics Specialist

Cases involving cryptocurrency, offshore accounts, or assets held in third-party names require a licensed investigative firm with digital forensics capabilities. Physical surveillance can document property or vehicles registered in other names, identify asset movements, and corroborate financial discrepancies with real-world evidence.

On the digital side, specialists use certified forensic platforms — Cellebrite, EnCase, and Magnet Forensics — to recover deleted financial files, examine device activity, and trace cryptocurrency wallet addresses across blockchain ledgers.

Prudential Associates, a Rockville, MD-based digital forensics and investigations firm operating since 1972, combines Certified Fraud Examiner (CFE) credentials with advanced blockchain analytics to uncover hidden digital assets, including cryptocurrency holdings that standard discovery typically misses. Their team assists attorneys in identifying which financial institutions or exchanges to subpoena based on forensic findings. Certified examiners have testified as expert witnesses in state and federal court proceedings.

Key Methods and Tools for Uncovering Hidden Assets

Tax Return and Public Records Analysis

IRS transcripts are a foundational resource. The IRS provides several transcript types: the wage and income transcript covers W-2s, 1099s, and other information returns for up to 9 prior tax years, while the record of account transcript covers the current year plus 3 prior years. Comparing multiple years of returns can reveal sudden income drops, new deductions, or business entities that emerge at the same time as divorce planning.

Public records add another layer:

- Property deed records — reveal real estate holdings not voluntarily disclosed

- UCC filings — searchable through state databases (NY Department of State, California Secretary of State) and can reveal business assets and secured interests

- Business entity records — corporate filings identify ownership stakes in companies that may never appear in sworn disclosures

When these sources are stacked against sworn financial disclosures, gaps and contradictions become hard to explain away — which is precisely when discovery disputes gain traction.

Digital Forensics and Cryptocurrency Tracing

Digital forensics tools can recover deleted financial files and examine device activity. In divorce investigations, blockchain analytics has become a particularly consequential capability — tracing wallet addresses across public ledgers, identifying connections to mixing services or exchange accounts, and linking on-chain activity to real-world entities.

Major cryptocurrency exchanges — including Coinbase and Binance.US — publish legal process procedures and can be served with civil subpoenas through their registered agents. Courts regularly compel exchanges to produce account records in civil proceedings, making this a well-established route for attorneys.

Subpoenas and Third-Party Records

Subpoenas are powerful precisely because they go around the concealing spouse. A broad range of third parties can be compelled to produce records, including:

- Banks and credit unions

- Investment and brokerage platforms

- Payroll processors and employers

- Cryptocurrency exchanges

- Business partners and accountants

For offshore accounts, the Hague Evidence Convention provides a mechanism for requesting evidence abroad, though Article 23 allows some participating states to limit pre-trial document discovery.

Common Mistakes to Avoid When Searching for Hidden Assets

Three missteps can seriously undermine a hidden-asset investigation — or expose you to legal liability before it even begins.

Acting too late. Assets can be moved, converted to cash, or transferred to third parties quickly once a spouse decides to file. Start preserving documents and retain legal counsel as early as possible.

Accessing accounts or devices without authorization. The ABA has specifically warned that accessing a spouse's personal email without consent can violate federal law — including the Federal Wiretap Act (18 U.S.C. § 2511), the Stored Communications Act (18 U.S.C. § 2701), and the Computer Fraud and Abuse Act (18 U.S.C. § 1030).

The consequences are serious: illegally obtained evidence can be inadmissible, expose you to personal liability, and damage your credibility with the court. Always work through legal channels.

Accepting disclosures at face value. If your spouse controlled marital finances, their sworn disclosures deserve independent verification. Discrepancies in reported income, property values, or business performance should be formally investigated, not dismissed as minor variations.

Legal Consequences for a Spouse Caught Hiding Assets

Courts do not treat financial concealment lightly. The consequences range from financial penalties to criminal charges.

Civil penalties under California law illustrate the range:

- California Family Code § 1101 authorizes 50% of an undisclosed or transferred asset, plus attorney's fees and court costs, for breach of fiduciary duty

- For fraud, oppression, or malice, the court can award 100% of the concealed asset to the innocent spouse

That 100% outcome isn't theoretical. In In re Marriage of Rossi (2001), a California court awarded a husband 100% of lottery winnings his wife had concealed during dissolution proceedings.

More severe consequences for egregious concealment:

- Contempt of court charges, carrying fines or potential jail time

- Perjury charges for lying on sworn financial disclosures — a discovery response carries the same legal consequences as lying under oath in court

- Fraud charges in cases involving deliberate, systematic concealment

Concealment doesn't end the risk once a divorce is finalized. California Family Code § 2122 allows courts to set aside divorce judgments based on fraud, perjury, or failure to comply with disclosure requirements — meaning a settled case can be reopened years later if hidden assets surface.

When courts find intentional fraud, they don't simply adjust the split. They revisit original awards entirely, and the spouse who concealed assets often ends up with less than they would have received through honest disclosure.

Frequently Asked Questions

How do I find hidden assets during a divorce?

Start by preserving financial records before assets can be moved, then use formal discovery tools — interrogatories, subpoenas, and depositions — to compel disclosure. For complex cases involving business interests or cryptocurrency, forensic accountants and digital forensics specialists are often essential.

What shows up in an asset search?

A professional asset search typically surfaces real property holdings, bank and investment accounts, vehicles, business ownership interests, liens, and UCC filings. Advanced searches (particularly those involving digital forensics) can also identify cryptocurrency wallets, exchange accounts, and indicators of offshore holdings.

How do I find out if my spouse has a secret bank account?

The most reliable methods are subpoenas to financial institutions, forensic review of credit reports (which list open accounts), and analysis of tax returns and bank statements for unexplained cash flows. Loan applications are particularly useful since they list all accounts and assets at the time of borrowing.

Is discovery worth it in a divorce?

Discovery is worth pursuing whenever significant assets are at stake. Lying in discovery responses constitutes perjury, and courts can sanction the concealing spouse with disproportionate asset redistribution, fee awards, and even criminal referrals.

What assets cannot be touched in a divorce?

Separate property — assets owned before marriage or received as individual gifts or inheritances — is generally not subject to division. The key exception is commingling: when separate and marital funds mix, separate property can convert to marital property. Rules also differ between community property states (California) and equitable distribution states (New York).

How do I look up a person's assets?

Property deeds, business entity filings, UCC liens, and court judgments are publicly searchable. A comprehensive search, however, requires legal discovery tools or a licensed investigative firm with access to professional-grade databases and, for digital assets, blockchain analytics capabilities.