Many people assume a financial review is straightforward. Pull bank statements, check tax returns, done. But experienced investigators know that concealment is deliberate and often structured — through shell companies, trusted relatives, offshore accounts, or cryptocurrency wallets that leave no obvious paper trail.

This guide covers the warning signs of concealment, a step-by-step search process, specialized investigative techniques, and when professional help becomes necessary rather than optional.

Key Takeaways

- Hidden assets appear in many forms: cash, real estate, offshore accounts, business interests, and cryptocurrency

- Warning signs include lifestyle inconsistencies, unexplained transactions, restricted account access, and sudden income drops

- Effective searches start with tax returns and bank statements, then escalate through formal legal discovery

- Forensic accounting, digital forensics, OSINT, and blockchain tracing dramatically improve detection odds

- Cases involving businesses, offshore accounts, or digital assets require professional expertise to produce court-admissible findings

Warning Signs That Assets Are Being Hidden

Catching red flags early matters. Once an investigation formally begins, a subject who suspects scrutiny may move, transfer, or further conceal assets. Identifying warning signs before that happens preserves your options.

Key behavioral and financial red flags:

- Cash withdrawals, wire transfers, or payments to unknown recipients that don't match documented expenses

- Expensive travel, purchases, or gifts during a claimed period of financial hardship

- Sudden password changes on joint accounts, missing financial statements, or withheld documents

- Dramatic revenue drops or inflated business expenses appearing just before or during a legal dispute

According to AAML's 2024 business valuation paper, a controlling spouse may manipulate records, delay income, create sham liabilities, or transfer assets to friends and family — patterns that rarely surface without a structured investigation.

Assets frequently move to trusted third parties: family members, business partners, or shell companies. This means any serious investigation needs to extend beyond the primary subject's immediate financial records.

None of these signs confirm concealment on their own. Together, they build a factual basis for escalating to formal legal discovery or engaging a forensic investigator to examine records in depth.

How to Find Hidden Assets: Step-by-Step

Step 1: Build a Financial Profile of the Subject

Before touching a single document, build a complete background picture. Gather the subject's full legal name, Social Security number, date of birth, known addresses, employer history, close associates, and business affiliations.

From there, map the known financial footprint: shared and individual accounts, property records, investment accounts, and business interests. This baseline is what you'll measure discrepancies against throughout the investigation.

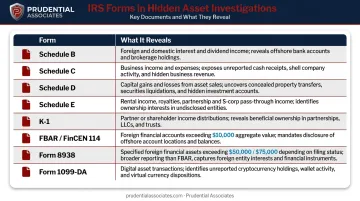

Step 2: Review Tax Returns and Financial Documents

Tax returns are effectively an asset index. Start with the most recent 3–7 years and cross-reference every schedule:

| Form | What It Reveals |

|---|---|

| Schedule B | Interest, dividends, and foreign account disclosures |

| Schedule C | Sole-proprietor income and business deductions |

| Schedule D | Capital gains from asset sales, including digital assets |

| Schedule E | Rental income, royalties, partnership and S-corp interests |

| Schedule K-1 | A partner's share of income, deductions, and credits |

| FBAR / FinCEN 114 | Foreign accounts exceeding $10,000 at any point during the year |

| Form 8938 | Specified foreign assets over $50,000 (year-end) or $75,000 (anytime) for single filers |

| Form 1099-DA | Digital asset proceeds from broker transactions |

Discrepancies between stated income and actual spending patterns are where concealment becomes visible.

Step 3: Analyze Bank Statements and Cash Flow

Those discrepancies often show up first in cash flow. Pull all accessible bank and credit card statements and look for:

- Large cash withdrawals with no clear purpose

- Transfers to recipients with no documented business relationship

- Overpayments on debts (which function as hidden savings)

- Payments to individuals that lack any supporting invoice or agreement

Forensic examiners apply three indirect methods to detect income from unknown sources: the net worth method, the expenditures method, and the bank deposits method. Each reconstructs financial activity from a different angle to identify gaps between known funds and actual spending.

Step 4: Search Public Records and Digital Footprints

Public records are underused in asset searches. A systematic search should cover:

- Property deeds and real estate transfer records

- Vehicle registrations

- Business entity filings (LLCs, corporations, DBAs)

- Court records and judgments

- UCC filings, which can reveal collateral and financial relationships

Social media and digital activity are equally valuable when obtained through proper legal channels. The ABA's hidden assets guide specifically calls out TikTok and Instagram as platforms where lifestyle evidence frequently contradicts a subject's stated financial position.

Step 5: Use the Formal Legal Discovery Process

In divorce and civil litigation, formal discovery tools give you legal teeth:

- Interrogatories — pin down undisclosed accounts, business interests, and financial relationships before depositions

- Requests for production — compel disclosure of bank records, tax filings, and business financials that wouldn't be volunteered otherwise

- Depositions — lock in sworn testimony from the subject and key witnesses, creating a record that's difficult to walk back

- Subpoenas — go directly to financial institutions, employers, accountants, and business partners when voluntary disclosure falls short

Discovery abuse carries real consequences. California's In re Marriage of Feldman established that failure to comply with financial disclosure duties can trigger mandatory monetary sanctions and attorney fee awards under California Family Code §2107(c).

Key Techniques for Uncovering Hidden Assets

Basic document review catches obvious discrepancies. Specialized techniques find assets that were deliberately structured to avoid detection.

Forensic Accounting Analysis

Forensic accountants reconstruct a subject's true financial picture using the net worth, expenditures, and bank deposits methods — the same indirect proof methods the IRS uses in criminal tax investigations. When the numbers don't reconcile, income from unknown sources becomes apparent.

They also identify subtler patterns within financial statements:

- Unusual bonuses or compensation timing

- Above-market wages paid to relatives

- Deferred income or understated receivables

- Inflated liabilities that reduce apparent net worth

The ACFE's 2024 Report to the Nations, analyzing 1,921 fraud cases, found that 89% of fraudsters used active concealment methods — including fraudulent documents (41%), altered physical records (37%), and falsified electronic records (31%). These patterns require trained examiners to detect.

Digital Forensics and Social Media Intelligence

Digital forensic examiners recover deleted financial records, email chains, text messages, and device data that reveal undisclosed accounts or transactions. This evidence is particularly valuable when a subject has intentionally wiped records.

Prudential Associates' certified examiners use Cellebrite, EnCase, and Magnet Forensics (industry-standard tools) to conduct forensically sound acquisitions suitable for courtroom presentation. Their process covers data extraction, analysis, and formal reporting at every stage.

On the SOCMINT side, Certified Social Media Intelligence Experts on staff analyze activity across Facebook, LinkedIn, Twitter, Snapchat, TikTok, and Instagram. This work surfaces lifestyle evidence — travel posts, purchase behavior, high-end dining — that directly contradicts claimed financial hardship.

Social media evidence must be properly authenticated under Federal Rule of Evidence 901 to be admissible, which is why certified analysis matters.

Cryptocurrency and Digital Asset Tracing

Cryptocurrency wallets and exchange accounts are increasingly used to conceal wealth. As Bloomberg Law reported, digital currencies have created new ways for parties to hide money in divorce proceedings.

Starting with the 2025 tax year, brokers must issue Form 1099-DA reporting digital asset proceeds, creating a traceable paper trail. Exchange-reported transactions are only the beginning, though — wallets, peer-to-peer transfers, and mixing services require deeper analysis.

Blockchain analytics platforms allow trained investigators to:

- Trace wallet addresses and transaction histories across multiple blockchains

- Identify mixing and tumbling services used to obscure fund origins

- Link wallet activity to real-world identities through on-chain and off-chain data correlation

- Flag connections to darknet markets or sanctioned entities

Prudential Associates' cryptocurrency investigation team conducts transaction tracing, wallet identification and attribution, and pattern analysis to build evidence suitable for legal proceedings.

Property Appraisal and Business Valuation

Undisclosed or undervalued property is a common concealment vehicle. Assets that may never appear in voluntary disclosures include:

- Real estate held under LLCs or third-party names

- Collectibles, fine art, and jewelry

- Intellectual property and licensing rights

- Stock options and restricted stock units

In business cases, a valuation expert can identify whether income was suppressed through inflated expenses, misclassified personal expenditures, or deferred revenue — tactics documented in AAML's 2024 guidance on business valuation manipulation. Professional valuation of business interests and restricted stock units often reveals six- and seven-figure discrepancies that voluntary disclosures routinely omit.

Common Mistakes to Avoid

- Build the baseline first — jumping into document requests without a complete financial and personal profile leads to missed assets and wasted legal resources

- Don't assume — follow the evidence — proceeding from assumption rather than documented leads risks discovery abuse and sanctions against your client

- Account for non-obvious asset categories — investigators routinely overlook stock options, restricted stock units, deferred compensation, tax carryovers, and intellectual property, all of which carry real value:

- Stock options and restricted stock units (RSUs)

- Deferred compensation arrangements

- Tax loss carryovers and retained earnings

- Intellectual property and licensing rights

- Know when to bring in professionals — surface-level screening can work early in a case, but business ownership structures, offshore accounts, and digital assets require forensic-grade investigation; incomplete findings that won't hold up in court are worse than no findings at all

Cases involving any of these categories benefit from certified forensic examiners and investigators who can document findings to evidentiary standards.

When to Bring in Professional Investigators

Professional investigators move from optional to necessary when:

- The subject owns a business with manipulated records

- Offshore accounts or foreign assets are suspected

- Cryptocurrency or digital assets are involved

- The value of potential hidden assets justifies the investigation cost

The distinction between what a forensic accountant provides versus what a full-service investigative firm provides matters here. Forensic accountants analyze financial documents and produce court-ready reports. A firm like Prudential Associates adds field surveillance, device forensics, OSINT, social media intelligence, and cryptocurrency tracing — capabilities outside a forensic accountant's typical scope.

Prudential Associates offers comprehensive Asset Determinations services covering bank accounts, brokerage accounts, real property, motor vehicles, and other assets, with an estimated 80–95% effectiveness rate at locating all accounts. Investigations extend to subjects and accounts both domestically and overseas.

The team brings specialized credentials to every engagement:

- Certified Fraud Examiners (CFE) for financial document analysis

- Certified Social Media Intelligence Experts (CSMIE) for digital footprint tracing

- Blockchain analysts using specialized platforms for cryptocurrency tracing

With CEO Jared Stern having testified as a fact witness in 500+ court cases, the firm's findings are structured to hold up under legal scrutiny from the start.

Frequently Asked Questions

How do I find out if my spouse is hiding assets?

Start by reviewing joint tax returns and bank statements for unexplained transactions, and watch for lifestyle inconsistencies or restricted account access. If red flags appear, escalate to a forensic accountant or private investigator — early action prevents evidence from being moved or destroyed.

How do you discover hidden assets in divorce?

Formal discovery tools (interrogatories, subpoenas, depositions, and requests for financial document production) are the primary legal mechanism. Forensic accounting and digital asset investigations supplement discovery in complex cases involving business ownership or cryptocurrency.

How do you prove someone is hiding assets?

Proof is built through documentary evidence (bank records, tax returns, financial statements), expert analysis identifying income from unknown sources, and sworn deposition testimony. Courts treat deliberate concealment as fraud, which carries serious penalties including contempt, sanctions, and potential redistribution of hidden assets.

Can a forensic accountant find hidden accounts?

Yes. Forensic accountants are trained to trace funds, identify undisclosed accounts, and reconstruct financial activity using indirect proof methods. They can also identify offshore account discrepancies through FBAR and Form 8938 reporting irregularities.

What counts as a red flag in forensic accounting?

Common red flags include unexplained deposits or transfers, income that doesn't match lifestyle, inflated business expenses, wages paid to relatives without clear business justification, and large cash transactions inconsistent with known financial activity.

What does a forensic accountant cost for a hidden asset investigation?

Costs vary based on document volume, number of accounts and entities, business valuation scope, cryptocurrency complexity, and whether expert testimony is required. In high-value cases, the financial recovery from uncovering hidden assets typically outweighs investigation fees.